Living Civilization Lens

Through the four-fields lens

The Coordination Geometry framework reads a company through four pillars (Capital, Information, Innovation, Trust) and four abstract fields (Tribal, Jurisdictional, Cultural, Economic), with each pillar's output bounded by what its native reality test has actually confirmed. Capital is Stock × Velocity → Work. Information is Data × Verification → Proof. Innovation is Ideas × Experimentation → Solutions. Trust is Agreements × Validation → Commitment. Debt arises in any pillar when the system treats unvalidated potential as realized output. AAOI is an unusually literal case for this framework, because the company's physical product is the substrate of one of its core dynamics. Optical transceivers are the rails over which capital velocity moves in the post-2024 AI economy: bandwidth between GPUs, between racks, between data centers is the medium through which value transfers in inference and training. AAOI does not just participate in AI infrastructure. It manufactures the physical infrastructure of velocity itself. Reading the company through the four fields produces a clear pattern. AAOI is selling a wealth-coordination product through a debt-coordination corporate structure, and almost every visible tension resolves to that single misalignment.

Tribal field: founder continuity carrying workforce gravity it does not describe

The Trust pillar does the structural work in AAOI's Tribal field, and it does the work in two directions that do not yet meet. Thompson Lin's 29 years of unbroken founder, CEO, and Chairman tenure is a substantial Trust accumulation in the Sugar Land identity layer. Agreements have been ratified, validated, and re-ratified across nearly three decades of public and private commitments. Continuity at that depth is rare in hardware and almost extinct in public-company hardware. It is the kind of provenance that, in a healthy Trust pillar, lowers coordination cost by removing the need to renegotiate institutional identity at each cycle. The cable operator relationships, including the recent Mediacom DOCSIS 4.0 partnership, sit inside that same accumulation. They are real and durable Trust deposits in a single regional ecosystem.

The tension surfaces at the level of workforce provenance. The largest single concentration of AAOI's people, 2,927 employees, is in Ningbo. Houston has 508. Taipei has 1,274. Atlanta R&D has 64. The brand identity is Texan. The workforce center of gravity is Chinese. This is not a hidden fact, but it is rarely the lead in AAOI's public communications, where the Sugar Land expansion and CHIPS-aligned reshoring story carries the narrative weight. In framework language, the Tribal field is being addressed through one provenance signature while the actual labor coordination operates under a different one. The community license AAOI holds in Texas is real. The community license it holds in Ningbo is the one that actually produces most of the volume, and that license is held under conditions the Sugar Land narrative does not describe. This is not necessarily a Trust pillar breakdown. It is a Trust pillar asymmetry that becomes a structural liability the moment either sovereign frame above it tightens.

Jurisdictional field: a pinch point between two sovereign frames whose alignment is being assumed

The Jurisdictional field is where AAOI's coordination geometry shows its sharpest tension. The pattern is a Jurisdictional distortion produced by partial Trust pillar engagement with two sovereign frames at once. The company files as a Delaware corporation, accepts a $20.9M Texas Semiconductor Innovation Fund grant, positions itself for CHIPS Act benefits, and presents itself in US public markets as a domestic industrial reshoring story. At the same time, 44.8% of 2024 revenue came from products manufactured in China, up from 19.9% in 2023 and 23% in 2022. The China cost basis is not just present. It is expanding during precisely the window in which the US-facing narrative is moving in the opposite direction.

The tariff exposure makes the asymmetry visible in cash terms. The additional 10% tariff on Chinese imports imposed in 2025 hits AAOI's cost base directly, and management stated on the Q1 2026 call that they cannot estimate the timeframe for tariff refund recovery. That is an honest disclosure of an unhedged sovereign exposure. The ISS Governance QualityScore of 7 on the 10-point decile scale, with the Audit pillar at 10 and Shareholder Rights at 8, indicates that the governance system surrounding these jurisdictional exposures is rated as carrying meaningful structural risk relative to peers. None of this means the company is operating outside legal frames, or even unusually for a hardware firm with Asian manufacturing roots. It means the Trust pillar's validation function is being asked to span two sovereign frames whose alignment cannot be assumed, and the company's narrative has been positioned as if one of those frames had already won.

Economic field: debt-based capital coordination expressed as growth

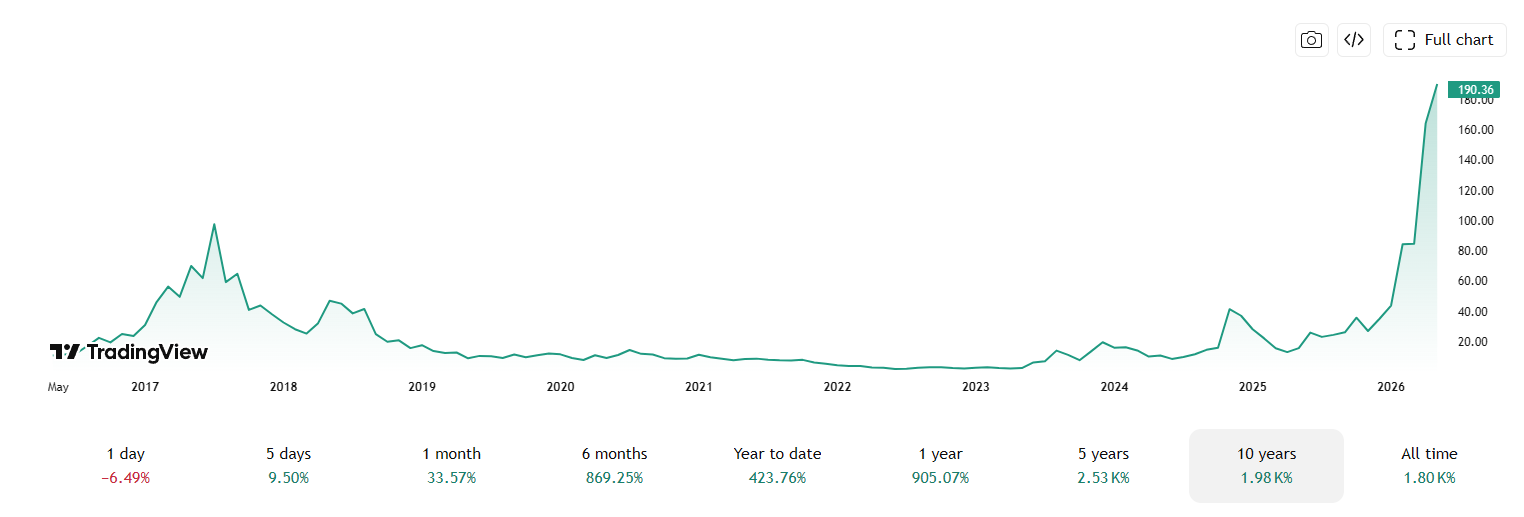

The Economic field is where the framework's wealth-versus-debt distinction reads AAOI most cleanly, and the reading is unambiguous. The Capital pillar is doing all the visible structural work, and the form it is taking is debt-based coordination expressed through equity dilution rather than through fixed-income instruments. Across roughly 14 months ending in May 2026, AAOI raised approximately $382.4M in a public equity offering, $125M in 2.75% convertible notes due 2030, and established a new $600M at-the-market issuance program. Over $1B of dilutive capital activity is being deployed against a market capitalization currently near $12B. The company has never paid a cash dividend in 13 years of public existence, so the 0% line on the long-term dividend chart is a structural identity, not a cyclical absence. All retained value plus all newly issued claims fund forward expansion against imagined future demand. In the framework's vocabulary, this is Capital compressing future production into present spending, which is the precise definition of the debt form in the Capital pillar.

The customer concentration profile makes the diagnosis sharper. Per the 2025 10-K, Digicomm International represented 53.1% of revenue, Microsoft 28.8%, and the top 10 customers 96.6% of total revenue. The 2017 precedent is directly material. Amazon was 54.6% of revenue and Microsoft 18%. Amazon shifted procurement, and the stock fell from above $100 to near $2 over six years. The Amazon Customer Warrant signed in March 2025, with up to 7.945 million shares at a $23.6954 strike tied to up to $4B in discretionary purchases through March 2035, is structurally a procurement framework with vesting incentives. The word "discretionary" is load-bearing. It is not a take-or-pay contract. It is an agreement whose validation depends entirely on Amazon's forward choices, which is the exact mechanism that failed in the 2017 cycle. The framework's vocabulary names this directly: relationships that look like Commitment but lack genuine validation under stake produce Trust Debt rather than Trust, and coordination cost spikes when the deferred validation moment arrives.

The signals of speculative crowding sit on top of the underlying structure. Defiance Capital launched a 2X daily leveraged single-stock AAOI ETF in April 2026. Insider selling of approximately 606,000 shares occurred at 52-week highs. Q1 2026 institutional ownership declined approximately 24.25%. The framework reading is direct. The activation equation Stock × Velocity → Work is being attempted, but Stock is being manufactured through dilution faster than the Work term has been validated to absorb it. Real industrial capacity is being built. The financing form is extracting against an imagined 2027 and 2028 margin profile that has not yet been delivered.

Cultural field: data emission running ahead of verification

The Cultural field is where the Information pillar's activation equation, Data × Verification → Proof, reads most clearly, and the diagnosis is that data emission is currently outpacing verification. AAOI's tagline shift from "leading provider of fiber-optic networking products" to "leading provider of advanced optical and HFC networking products that power AI" is a deliberate and recent narrative repositioning. The speed-grade product progression from 100G to 400G to 800G to 1.6T is itself the marketing, an order-of-magnitude bandwidth narrative that maps directly onto the AI infrastructure thesis. At the substrate level, the claim is correct. Optical transceivers are the physical rails of capital velocity in the AI economy, and AAOI's vertical integration in laser fabrication is a genuine structural advantage during an industry-wide EML laser shortage that is constraining competitors' 800G ramps.

The verification gap shows up where the brand claim runs ahead of the operational reality it describes. The vertical integration narrative is presented as a solved problem, but management stated on the Q1 2026 call that material supply remains a live risk under active mitigation. The reshoring narrative carries the visual weight of the Sugar Land expansion, while the cost basis sits increasingly in Ningbo. The founder-continuity narrative implies patient capital and slow building, while the actual capital execution is among the fastest dilution sequences of any hardware issuer in the cycle. Two coherent stories are being told in parallel, and they describe incompatible companies. The Trust pillar's validation function would normally resolve which story is load-bearing, but during a narrative-driven price cycle the question is deferred rather than answered.

The legacy CATV identity is the cleanest indicator of the verification lag. Cable broadband was the entire identity of AAOI for two decades and remains roughly 44% of Q1 2026 revenue at $66.8M of $151.1M. Charter Communications' capex cycle is a material live exposure. None of this appears in current public communications with anything close to the weight of the AI infrastructure narrative. The Cultural field is doing what cultural fields do under narrative cycles: producing a forward-looking identity statement that the underlying coordination structure has not yet validated. In framework terms, this is Proof being claimed at a rate that exceeds what Data × Verification has actually generated, which is the Information pillar's debt form, the speculation gap. That is not deception. It is the standard pattern of cultural emission running ahead of structural confirmation in a momentum cycle. The framework's contribution at this point in the analysis is naming the gap clearly, so the reader can hold the AI infrastructure thesis and the cable broadband revenue base in the same picture without one cancelling the other.